.svg)

Stop the Presses

A Bit More Light for Spring Equinox

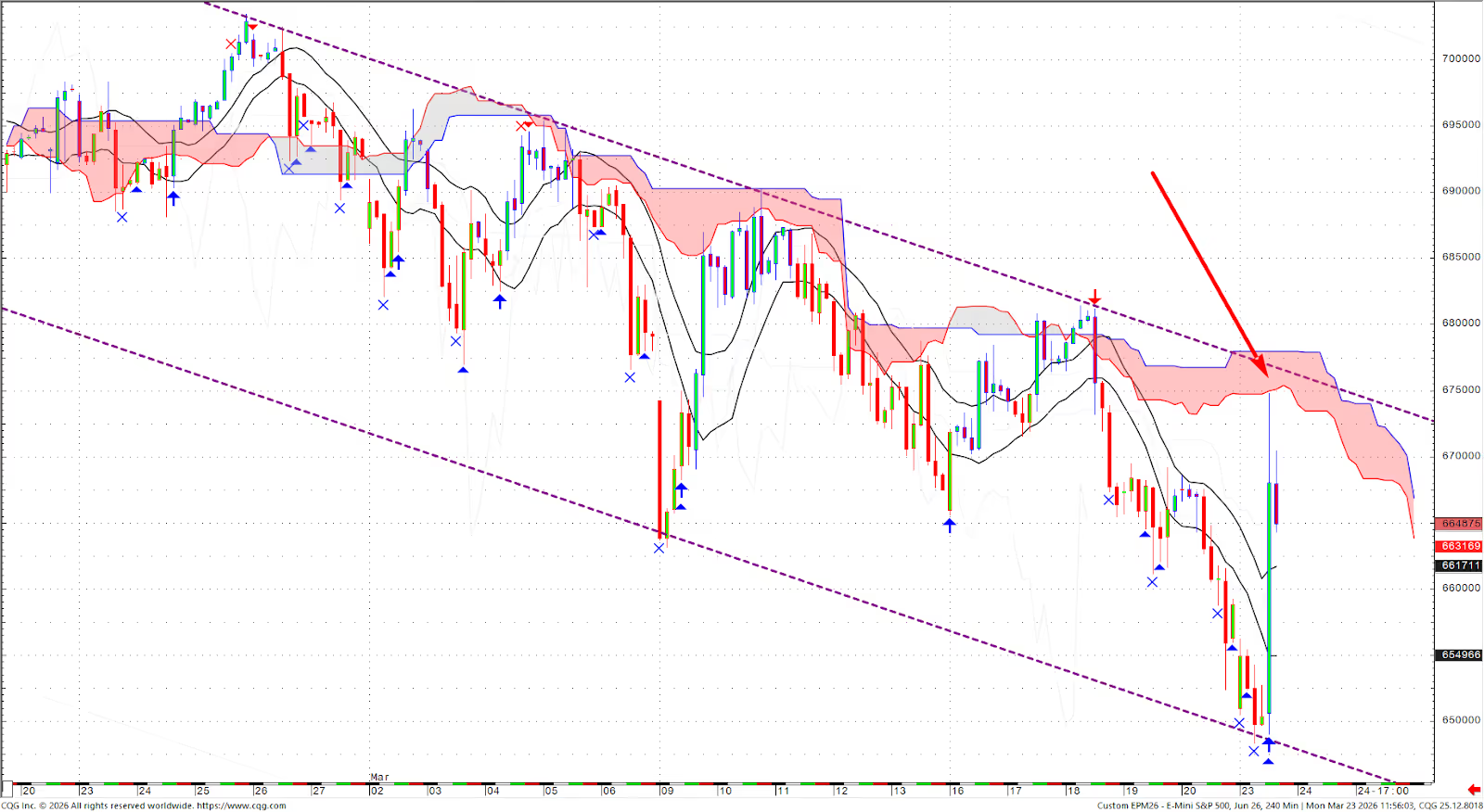

Soundbite: We interrupt your regularly scheduled programming to bring you a chart of price action. This picture is certainly worth a thousand words as it reveals a reversal level above which the conditions for risk assets would turn bullish.

President Trump’s announcement of a five-day ceasefire to conduct talks with the new (harder-line) Iranian government has injected a ray of sunshine into what has been a dark few weeks.

Below we present the 240-minute S&P futures chart going back to mid-April:

Where markets stop after a fast rise or drop is key. The cloud resistance, the red zone where selling pressure tends to emerge, is still intact (see red arrow), as is the downward channel that has formed (dotted lines) since before the February 28 invasion.

A break above both of these barriers will constitute a trend change currently near 6700 in the S&P 500 cash index. Until then, the market remains skeptical.

Throwing Out the Playbook

Soundbite: Consensus trades are under fire. Coming into the year, “smart money” was long silver, short the dollar, long emerging markets, and long the Treasury curve steepening trade. These trades are all underwater year-to-date, and gold is experiencing its worst month since its selling climax in October 2008. Hope remained for the hyperscalers, despite capital expenditures siphoning off their cash flow, but they too underperformed. Even within U.S. commodity stocks, basic materials and metals and mining are down for the year, although energy stocks have been massive winners. The question is whether those themes are permanently broken or will revive.

With positioning nearing extreme lows and heavily negative sentiment, the window for a market reversal is open. During the bounce, look closely at which stocks outperform. If leadership returns to those popular trades mentioned earlier, then new equity index highs cannot be ruled out. If investors use any bounce to reduce their holdings in those once-winning ideas, those trades will continue to lag. Take that as a signal to join them and get exposure down.

The answer to whether it is smart to continue holding those favored December trades may lie within the least popular themes. Let us use business development companies and listed private equity stocks as examples. In risk-off periods such as now, correlations go to one as everything is sold indiscriminately. Hedge funds and institutional investors are forced to reduce their overall exposure, and in doing so, buy back heavily shorted names (which is why those stocks could outperform during a selloff). Therefore, the fact that out-of-favor business development companies such as Blue Owl did not make new lows on Thursday and Friday, while the S&P was plunging, may be a false signal. However, the major private equity players (Blackstone, KKR, Carlyle and Apollo) bottomed out over a week ago, in what could be a significant reversal signal.

Anecdotally, we took note of JP Morgan and Goldman rolling out structured products to help investors hedge their exposures in private credit. The space has been hammered by gated redemptions and rising defaults, estimated at more than 9% at year-end 2025. There is an old stock market adage that if everyone in the market is clamoring for something, gladly give it to them. These events frequently coincide with periods of peak pessimism. Michael Burry quipped that “if the big banks are ‘offering’ you a way to make money, you’re the exit liquidity.” Additionally, because these instruments will increase liquidity to the asset class, doing so should ease a major investor concern. If pessimism lifts, it could have bullish repercussions for software stocks, a beleaguered sector that has quietly outperformed the market since a week before the Iranian conflict.

We are also aware of the bearish argument: JP Morgan has started to mark down software loans in private credit portfolios, creating a potential deleveraging problem. We believe the market may have already discounted this fear, although with $300 billion in loans to private credit, conditions could take a turn for the worse. Despite the clouds, Friday’s Federal Reserve H.8 report on commercial banks shows that loans to nondepository financial institutions continue to rise. Despite the war, loans continued to rise this month, and as of March 11, they stand at $1.92 trillion.

Bottom line: Look in the corners of the market for clues of shifting tides, especially over the next two weeks.

Compare and Contrast: Last Week’s Fed and ECB Meetings

Soundbite: Following last week’s Fed meeting and release of the March Summary of Economic Projections (SEP), we remarked in Pave’s Substack that we were surprised that the normal economic impact of higher oil prices was not reflected in a weaker GDP forecast. In fact, the median 2026 GDP estimate was higher than their December 2025 forecast for this year. The increase was especially surprising because their 2026 core inflation forecast (ex-food and energy) rose to over 4%, 1.5% higher than December’s estimate. The following day, the ECB’s press conference revealed a lower European GDP forecast due to the Iranian conflict, and warned that $120-$150 oil could trigger a recession lasting two quarters. Can both be correct?

Comparing the two press conferences from Jerome Powell and Christine Lagarde, we did find one area for common ground: both acknowledge that long-term inflation expectations are now susceptible to rise, unlike in 2021-2022, simply because consumers have had a recent experience of high inflation just a few years ago, compared to 2022 when the last bout of inflation was the 1980s. This is a critical point of agreement, and something investors will need to incorporate in their own forecasts. We discussed this point last week when we wrote that bonds will not be a viable hedge against stock selloffs driven by inflation worries and rate hike concerns.

There is undoubtedly a worry among both central banks that long-term inflation expectations could rise if short-term inflation stays high for a few months. Powell was clear in his remarks:

"The fact that consumers have experienced five years of above-target inflation, you worry that a shock could cause trouble for long-term inflation expectations."

At the very end of her press conference, Lagarde echoed Powell’s sentiment by adding this warning:

“Inflation expectations have a lot to do with the memory that people and corporates have of inflation back in 2022, and [back then inflation was a distant memory]. Now the memory is rather fresh because people have seen inflation. So, the reaction function that they will have in terms of investment…wage negotiations and…consumption is going to be informed by a fresher memory of inflation.”

Our overall view on Wednesday’s FOMC meeting is that Chair Powell took a tough stance to contain long-term inflation expectations, leading the market to believe there was a lower chance for policy easing. That seemed to be his overriding principle. Three key comments during his press conference:

- “No progress on inflation, no rate cut.”

- “Looking through oil prices depends on inflation expectations and the broader context of five years above [our two percent inflation] target,” and

- Last year's cuts have now brought funds to a “plausible estimate of neutral.”

His tone set the stage for an asymmetric outlook, tilted toward fewer cuts.

Powell outlined the view among FOMC members that the improved GDP forecast stood on stronger footing thanks to recent productivity strength; these gains were not from AI, but possibly “due to adjustments during the pandemic.” Turning to the ECB, domestic demand is expected to be supported by ongoing fiscal stimulus related to defense and infrastructure spending—mostly driven by Germany—assuming the crude spike is transient. However, the ECB still predicts weaker 2026 real GDP based on the hit to consumption from higher crude.

The European Central Bank cut its baseline GDP forecast by 0.3% this year compared to the Fed, which raised its GDP forecast by 0.1% for 2026. The ECB expects crude to stay around $90 this quarter, before energy prices fall sharply thereafter.

Whereas the Fed did not quantify what would occur if the Middle East conflict escalated, the ECB offered two alternative outlooks: one severe scenario with $120 oil (1-standard deviation move) and one adverse scenario peaking at $150 crude (2-standard deviation move) this quarter. In both severe and adverse cases, the economy would contract for two consecutive quarters through Q3, putting the continent in a recession from which real GDP is forecast to bounce back strongly toward its 2% trend.

The ECB recession scenario was buried in a lengthy analysis posted on their website, and Lagarde avoided any mention of recession. Our guess is that the Fed is also looking at similar depressed growth scenarios in case the economy is burdened by a sustained bout of triple-digit crude prices. At the outset of the conflict three weeks ago, we discussed our rule that if oil is $130 in April or May, it constitutes a year/year doubling of energy prices, crossing a critical recession threshold.

Because no one knows the path of crude oil into the next two months, it was prudent for Powell and Lagarde to sidestep the dark side and stay in a small portion of light. Our guess is that they will cross that $130 bridge only if we get there, not before.

What to Look for This Week

(All times E.S.T.)

- Tuesday, March 24 at 10:00 a.m. Conference Board Consumer Confidence for March. Due to the rapid change in oil, the confidence reports this week are the most important datapoints. This poll has a March 17 cutoff date, so it will not be a complete sample after the invasion, but a good look. The Current and Expected Financial Situation will be a focus, as will the Expectations Index subcomponents for income, business, and labor market conditions. Consumers’ write-in responses continue to be dominated by inflation, and the cost of goods. Another focus: respondents’ views about the likelihood of a recession over the next year. Friday March 27 at 10:00 a.m. University of Michigan Survey of Consumers Final for March. The preliminary report captured only 9 days of data for March, yet there was already a visible impact on Confidence and Long-term Inflation Expectations. Confidence hit its lowest level of the year at the preliminary March release. An additional two weeks into a period of high gas prices will be enlightening. As the Survey said, “Gasoline prices have exerted the most immediate impact felt by consumers, though the magnitude of passthrough to other prices remains highly uncertain.”

- Wednesday, March 25 at 7:00 a.m. Mortgage Bankers Association Purchase Index for the week ending March 20. In January, the MBA Purchase Index hit a 3-year high and promptly came off hard into February. Notably, the March 6 and 13 readings were strong, reversing the weak trend, which was after the Iranian news and the ensuing crude spike. Therefore, we are keen to see this week’s number.

- Thursday, March 26 at 8:30 a.m. Initial and Continuing Claims for the week of March 14. We track the four-week average of Initial Claims, which has improved for three weeks straight despite the weak February Nonfarm Payroll print of -92,000. In fact, the four-week moving average of claims was elevated in February, but has been improving since, auguring for a better March payroll release.

FOMC Voters Speaking: Floodgates have opened. Tuesday, March 24 at 3:30 p.m. Governor Michael Barr speaks on the economic outlook. Wednesday, March 25 at 1:10 p.m. Governor Stephen Miran speaks about digital assets and at 3:30 p.m. on Thursday, March 26 he discusses the Fed Balance Sheet. Earlier that day, Governor Lisa Cook discusses financial stability at 1:00 p.m. Governor Philip Jefferson also speaks on Thursday at 4:00 p.m., followed by Governor Barr at 4:10 p.m. in a moderated discussion. Friday, March 27 at 8:40 a.m., Philadelphia Fed President Anna Paulson speaks on Macroeconomics and Monetary Policy. Tuesday, March 24 at 7:50 p.m. the minutes of last week’s Monetary Policy Meeting in Japan are released, where they kept rates steady. Governor Ueda in his press conference stated, “Cannot say how long it would take to judge whether energy supply shocks affect underlying prices…[the BoJ is waiting until] after the release of the April Tankan report on whether they fully capture the Middle East conflict impact.”

Earnings: Only 200 companies report this week, and very few companies of interest. KB Home (KBH) reports Tuesday, March 24 after market. Looking for insight on inventories and affordability. Wednesday, March 25 before market Paychex, Inc. (PAYX) and after market, Jefferies, Inc. (JEF) where we are looking for any color on private credit. Friday, March 27 before market, Carnival Corporation (CCL) on the consumer and oil markets. Could be the highlight in terms of information value for the entire week.

By Peter Corey

Risk Disclosure & Disclaimer

Copyright © 2026 Pave Finance, Inc., LLC and Peter Corey. All rights reserved.

The attached material is provided in partnership with Pave Investment Advisers, LLC (“Pave”), and is the opinion of Pave and Pave’s Chief Markets Strategist, Peter Corey. Distribution is being provided through a licensing agreement, and any further dissemination is strictly prohibited.

You are receiving this email because you opted in through our product or website.

You can update your preferences or unsubscribe from this list.

For Financial Professional Use Only

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security. There is no guarantee any investment recommendations will be successful and there is a risk of losing money.

We take protecting your data and privacy very seriously. Please see our privacy policy here.

Pave Investment Advisors, LLC is an SEC Registered Investment Advisor. Such registration does not imply any level of expertise.

Securities offered through Pave Securities, LLC – New York, NY. Member FINRA/SIPC. You can review Pave Securities LLC with FINRA’s BrokerCheck BrokerCheck.

Advisory Services are only offered through Pave Investment Advisors, LLC., an SEC Registered Investment Advisor which is an affiliate of Pave Securities, LLC.

Pave Securities, LLC and Pave Investment Advisors, LLC do not offer tax or legal advice.

The news, resources and articles available on this site are being presented for educational purposes only and should not be considered specific investment or planning advice applicable to each individual.

%20(1)%20(1).png)

%20(1).png)

.png)